How a Basic Income could Lower Housing Costs.

The inflationary effects of a basic income would allow central banks to raise interest rates, slowing the flow of money from the financial sector into asset bubbles like stocks and, crucially, housing.

One of the most common objections raised to a basic income is that house prices and rents will simply be raised and erase all the income gains, leaving people back where they started. Even if all other factors were held static it seems likely that competition between landlords and home sellers — and with those selling other asset classes — would act as something of a brake on price increases, preventing them from absorbing all of the increase in income.

But other factors won’t be held static. For a start there would be a decoupling of the labour and housing markets which would increase vendor-side competition in the housing market, since there would be a greater number of people who could quit their current job and move where housing is cheaper. This would compliment and overlap with the existing trend towards remote work. The increased spending power and arrival of new customers in country towns would then create more employment opportunities, making them even more attractive relative to the city. It would of course put upward pressure on regional house prices, but the spread of demand would lessen pressure on city markets.

In Australia we’ve recently got a sense of the short term limits of this effect, as the pandemic increased city-to-country transitions, especially along the east coast, causing house prices in regional areas to rise, often pricing out locals. But in the longer term new housing stock could easily be added in these areas — at lower cost than in the cities.

But there are other factors lurking behind those rural price hikes, the same factors which prevented a collapse of house prices in the city, despite the biggest economic contraction on record.

Part of it is the Jobkeeper wage subsidy and increased Jobseeker unemployment payments, and the government allowing people to access up to $20k of their retirement funds, and directly incentivising home building and improvement (my family and I were recently evicted so my landlord could renovate, which the government was incentivising to the tune of $25k).

But the bigger part is simply cheap credit. House prices have remained high for the same reason the stock market has remained high: Because interest rates are effectively below zero. In the US is what’s been called a “fed driven economy”. Cheap money for those who already have assets and/or a good credit rating has sustained and even expanded what was already a huge asset bubble. You can borrow money, buy tech stocks, bitcoin, gold, or some other relatively safe asset -like real estate- and watch the value rise at a rate which far outstrips the interest on your debt.

This wasn’t the goal of central banks but a side effect of them crashing rates, in a desperate attempt to stimulate business activity, and fend off a great-depression-like economic catastrophe. It hasn’t totally failed, or been a huge success. It’s hard to tease out the causality, but my suspicion is that fiscal policy is what has kept the deflationary spiral at bay. Monetary policy has helped by supporting that spending with bond purchases. Low interest rates, on the other hand, have mostly fuelled the credit driven asset bubble — which can never be a good thing in the long term. Sure some businesses might stay afloat that wouldn’t have otherwise, but putting money in consumers hands would have had a much more direct and powerful effect, without increasing the instability in the financial sector. Similarly there are those who have avoided selling their house because interest payments were low — but increasing their incomes instead of lessening these payments would have solved that problem too, without inviting leveraged speculative investment.

A basic income would likely be, overall, (though not exclusively) inflationary. This would allow central banks to raise interest rates from their current record lows. That would increase the cost of borrowing, including mortgages, which would discourage asset speculation, including housing. The higher we make the basic income the more spending power it puts into people’s hands and the less we need to stimulate the economy (and asset pricess) with cheap credit.

The hardest question, as usual, is what do we actually want to do? It seems unfair to punish those in the middle class who have invested heavily in housing as an asset, and who were encouraged to do so by policy makers. But the current situation punishes all those below this stratum, those looking to buy their first home, struggling renters, and finally the housing insecure and homeless.

Perhaps the goal of a catch-up period, where house prices hold steady (in adjusted dollars) while the economy and incomes grow around them is the consensus point we can settle on. We could even aim for modest growth in real terms, so long as growth in incomes and the economy as a whole outpaced this, meaning the percentage of income spent on housing would shrink.

To achieve this balancing act, however, we will need a clear picture of what got us to this point.

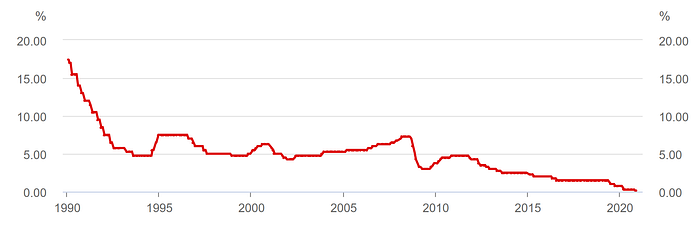

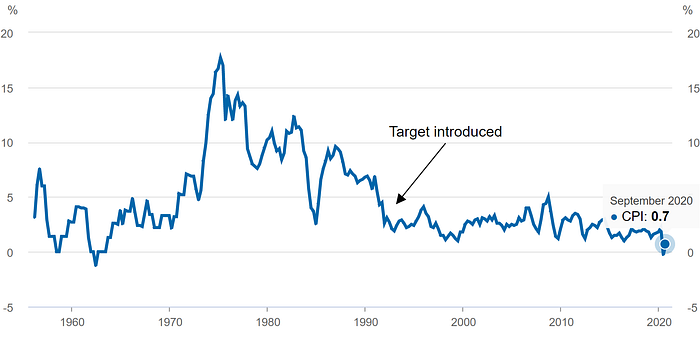

Even before the pandemic there had been a long period where overall conditions were predominantly deflationary, with inflation in Australia and many other major economies staying below the target range despite historically low interest rates. Attempts to raise these rates threatened to stall economic growth, so in 2008, then again from 2011 onwards they hit record low after record low.

This year rates dropped to just 0.1 of a percentage point. But even this combined with record government spending is only just enough to keep inflation in positive territory. But that’s just the pandemic right, suppressing spending? Actually not so much. Consumer spending is in fact at record highs in Australia! Especially spending on goods (and housing), rather than services. But with our mostly low case numbers, even restaurants are doing well.

There are deeper, long term trends at play that the pandemic has merely accelerated. Consider the following graphs from the Reserve Bank’s website

To understand these trends we have to properly understand the role of the banking sector in the economy, something mainstream economists are loath to do. Economists point out that on some level, money doesn’t matter. The point is the stuff it buys. This is of course, on some level, correct. The point of the economy is to make and distribute things, and provide services.

Obviously, however the people at the end of these supply chains need money with which to purchase these goods. So how does the current system -where there is no basic income- get them this money? Primarily through the labour market, which the banking sector and ultimately the central bank stimulates — or tries to — with lending.

But as productivity rises, less and less labour is needed to create the same — or even greater — outputs. This effect has been concentrated so far in the production of goods (rather than the provision of services), where globalisation and automation have combined to drastically reduce the need for labour, and increase productive capacity. There are now fears that automation will come for the service sector, too — but why should we be afraid? Why is having fewer people (and more machines) serving coffee and guiding tourists really such a terrible thing?

We are afraid because without jobs people become destitute. People go needlessly without, while productive capacity stands idle — the obscenity of housing insecurity and homelessness while many houses go unoccupied, for example. But basic income (which recent polling shows 58% of Australian’s already support, and only 18% oppose.) can fix this. Poverty can be abolished.

I don’t propose this strategy as a panacea. If the government got everything else wrong — in terms of public housing policy, the balance of infrastructure and immigration rates, and and so on — house prices and interest rates could rise simultaneously.

The capacity of the political class to fuck things up is inexhaustible. But sometimes, when enough pressure is applied, they can get things right, too. So it’s worth thinking about what that might look like.

We could increase minimum wages, and support unions who fight for higher pay in the private sector. We could increase government spending including both wages and employment numbers in the public sector. And we should do both those things.

But the simplest and best way to get money to people is to give people money.

So what about raising the unemployment payments? Yes. Good. That too.

Often it is assumed that these would be eliminated with the introduction of a basic income. But this need not be the case, these targeted and conditional payments could remain to lessen the income penalty for the involuntarily unemployed, and to incentivise and support (re)-entry to the labour market, so long and to the extent that we as a society think that’s desirable. Similarly student, parenting and disability payments could continue, stacking on top of the universal amount to support and incentivise socially valuable behaviour, and compensate for unfair disadvantage.

This would allow us to ramp the basic income in over time, rather than all at once. Everything else stays the same, and everyone with a Tax File Number and a bank account associated with that number gets a small but non-negligible amount, say $50 a week. Then when the sky doesn’t fall, we ramp it up towards (and maybe even beyond) a livable income while watching the effects on other indicators, like inflation, interest rates, inequality and housing prices, the labour market, adjusting the payment and/or other policy settings as we go.

This gradualist approach would allow us to balance the risks of doing too much against the risk of not doing enough — which is perhaps right now the greater danger.